Last updated date: March 27, 2026 | 4:43 pm

Table of Contents

Starting a business in the Philippines begins with choosing the right legal structure. You

can register as a sole proprietorship, a partnership, a corporation, or a one-person

corporation (OPC).

But which one is the best option for your business?

Choosing among the four common business structures in the Philippines dictates where you

register your business, the additional requirements, taxes, and the extent of liability.

Furthermore, registering your business is not just a legal requirement for businesses in the

Philippines. It is a strategic step that enhances credibility, fosters trust, and unlocks

market opportunities.

In this guide, we’ll explore the different legal business structures, shedding light on the

‘why” behind ‘what’ you choose. Read on to make informed decisions that will be your

passport to legitimacy and success.

TL;DR: What’s the Best Business Structure in the Philippines?

The best structure depends on your situation:

What is a business structure in the Philippines?

A business structure refers to the legal setup you choose when registering your business. It

establishes the framework that defines its ownership, management, tax obligations, and legal

responsibilities in the eyes of the government.

In the Philippines, your chosen structure affects key areas such as:

In simple terms, your business structure defines how your business operates legally and financially.

How to choose the right business structure

The best business structure depends on your goals, income level, risk tolerance, and

long-term plans.

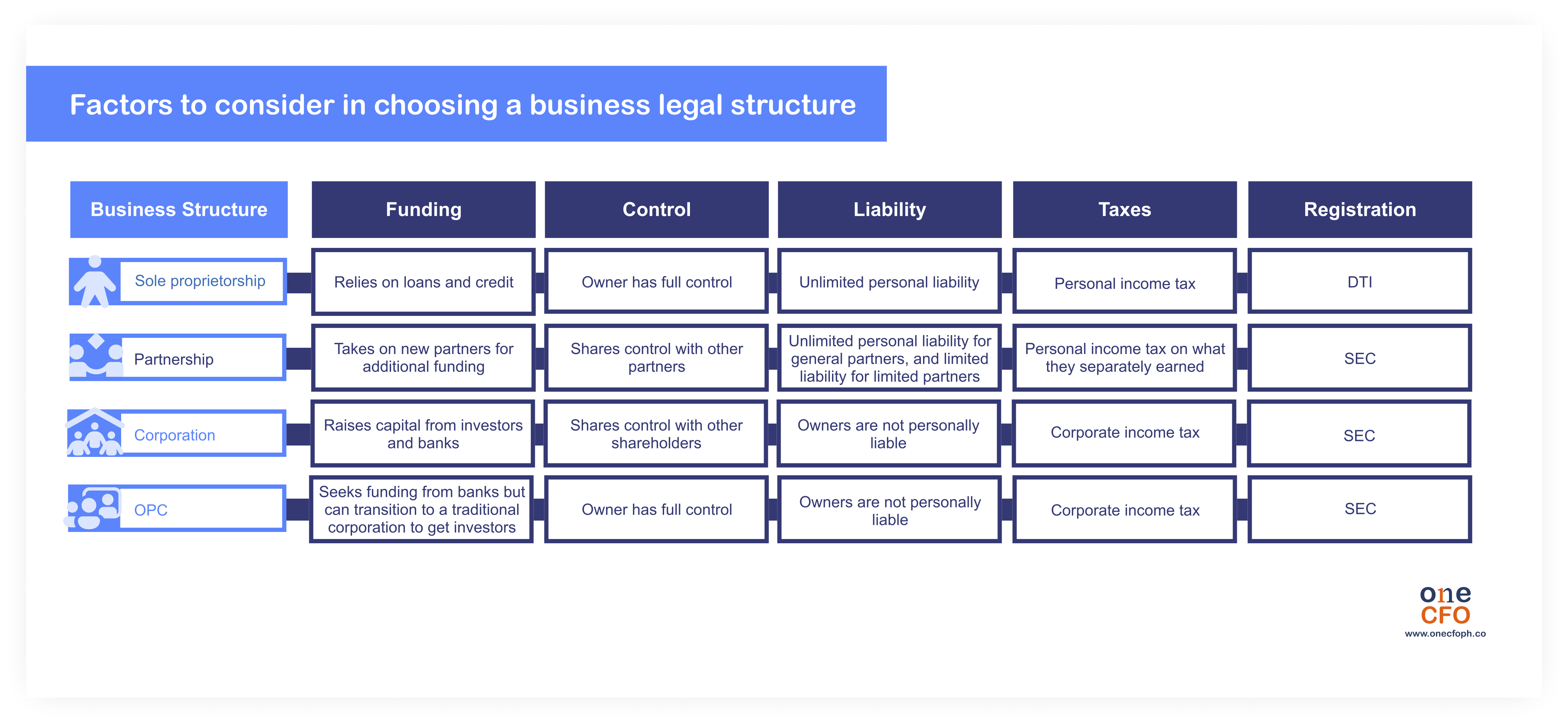

There are four main business structures in the Philippines. Here’s a breakdown of each,

including their pros and cons, to help you determine which one fits your business.

What is a Sole Proprietorship?

A sole proprietorship is the most common type of business structure because it's the

simplest to set up. Only a single individual owns and controls the business in a sole

proprietorship.

To register a sole proprietorship, the business owner must go through the Department of

Trade and Industry (DTI), the local government unit (LGU), and the Bureau of Internal

Revenue (BIR).

The DTI now requires online registration through their

Business Name Registration System for

faster processing.

How much is the tax for a sole proprietorship in the Philippines?

Sole proprietors in the Philippines pay income tax at either a graduated

rate or at 8%. The

graduated tax rates range from 0% to 35% depending on taxable income, while the 8% rate

applies only to those with yearly gross sales or receipts below Php 3,000,000.

If a sole proprietor’s gross sales/receipts exceed the ₱3,000,000 VAT threshold anytime

during the year, they must revert to the graduated income tax rates and register as a VAT

taxpayer.

To use the 8% tax rate, you must choose it when you register your business or when you file

your first quarterly tax return. Once chosen, it cannot be changed for the rest of the year.

Advantages of Sole Proprietorship

The main advantage of sole proprietorships is that owners have complete control over the

business. All final business decisions will be made by them, and they will keep and manage

the profits.

Another pro is that it’s the easiest to register for. Compared to other business structures,

a sole proprietorship requires the least paperwork: all you need to do is apply for a name

with DTI, get the necessary permits from the LGU, and register it with the BIR.

Disadvantages of Sole Proprietorship

The main disadvantage of sole proprietorships is that owners have no protection from the

business’s liabilities, as they are fully liable for all debts and losses incurred by the

business. Financial institutions can legally seize personal assets when the business suffers

losses or goes into debt.

Sole proprietorships also can’t distribute shares, making it hard to attract investors. You

can use other means, like business loans, to fund your business.

What is a Partnership?

If you start a business with at least one more person, where each contributes to the work

and shares the profit, then your business structure is a partnership.

In a partnership, each partner agrees to contribute money or service and gets a share of the

profit according to their capital contribution. Similarly, the partners distribute any

losses in the same proportion they share the profits.

Additionally, partners are liable for taxes on the income they earn separately. For example,

once the partners divide the profits among themselves, the amount a partner receives is now

subject to income tax, which that partner should pay accordingly.

Common examples of partnerships are law firms, accounting firms, and physician groups.

Because providing licensed professional services bears much weight and responsibility, their

businesses can only be partnerships with unlimited

liability to their stakeholders.

Business owners who want to establish a partnership should register with the Securities

Exchange Commission (SEC).

What are the two types of partnerships?

There are two types of partnerships: general partnerships and limited partnerships.

In a general

partnership, the partners evenly divide the profits among themselves. General

partners play a role in managing the business’s operations, but they also bear unlimited

liability in the company.

Unlimited liability means if the company or another partner takes on debt, all general

partners are liable for it. The partners’ assets are also unprotected.

Meanwhile, partners in a limited partnership are only liable

for the amount of their contributions. Limited partners also don’t have any management

rights to the business.

Advantages of Partnership

An advantage of a partnership is that you’re not alone in running the business. Partnerships

distribute the workload and decision-making among multiple individuals, reducing the burden

on one person.

Partnerships allow more resources. Partners can pool their financial resources and

expertise, potentially enabling the business to access more capital and talent. It also

helps if each partner has a different expertise, so one’s weakness can be another’s

strength.

In limited partnerships, limited partners enjoy asset protection, as they’re only

responsible for the amount of their investment.

Disadvantages of Partnership

Differences in opinion and conflicts among partners can arise, potentially leading to

disagreements or disputes that may be challenging to resolve. It may also disrupt the

business's harmony, affecting employee morale and overall productivity.

You also don’t have complete control over the business in a partnership. Partnerships

require consensus on major business decisions, which can slow decision-making.

While general partners enjoy greater profits and control, they bear more risk due to

unlimited liability. Each partner is responsible for the business’s debts and liabilities,

with their personal assets at risk.

What is a Corporation?

A corporation is a type of business

owned by two or more people who share ownership through shares of stock.

Corporations have a juridical personality separate from their stockholders. All stockholders

enjoy limited liability as they are only responsible to the extent of their shared capital.

Business owners register their corporations with the SEC. When establishing a corporation,

the SEC approves the authorized capital the company will

have, which is the maximum amount of shares the company can distribute.

How much is the corporate income tax?

The corporate income tax rate (CIT) in the Philippines is generally 25% for most domestic

corporations. This tax rate is imposed on a corporation's net taxable income after allowable

deductions.

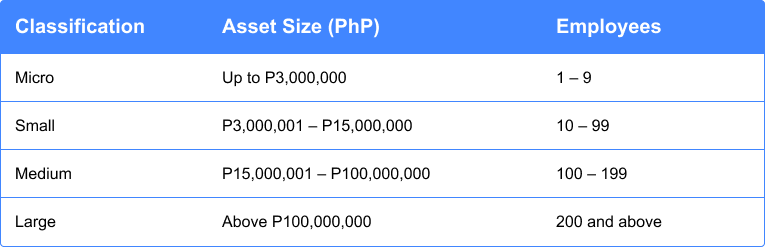

However, corporations classified as micro, small, and medium enterprises (MSMEs) may qualify

for a lower tax rate. If their net taxable income does not exceed ₱5 million and total

assets are not more than ₱100 million (excluding land on which the business’s office, plant,

and equipment are situated), they are taxed at 20% CIT.

Here is the MSME classification in the

Philippines:

What are the two types of corporations?

Businesses can choose to register as either a stock corporation or a non-stock corporation.

Advantages of a Corporation

The most apparent advantage of a corporation is that all stockholders have limited liability

for the business's debts, meaning their assets are protected.

Some corporations may also be exempt from income tax depending on

their purpose. This

includes non-stock, non-profit corporations organized for charitable, religious, or

educational purposes, subject to certain conditions under the law.

Corporations can often deduct a wide range of business

expenses from their taxable income. Here’s a good guide on the allowable tax deductions for

businesses:

A corporation is well-suited for businesses that want to grow quickly, as it can raise capital from investors. Being a corporation allows them to distribute equity to venture capital firms, helping them scale their operations.

Disadvantages of a Corporation

Setting up a corporation can be complex, time-consuming, and costly. Corporations must pay

registration fees, file annual reports, and maintain detailed corporate records.

They also face stricter regulations, including audits, corporate governance rules, and

disclosure requirements. This makes compliance more demanding and increases administrative

costs.

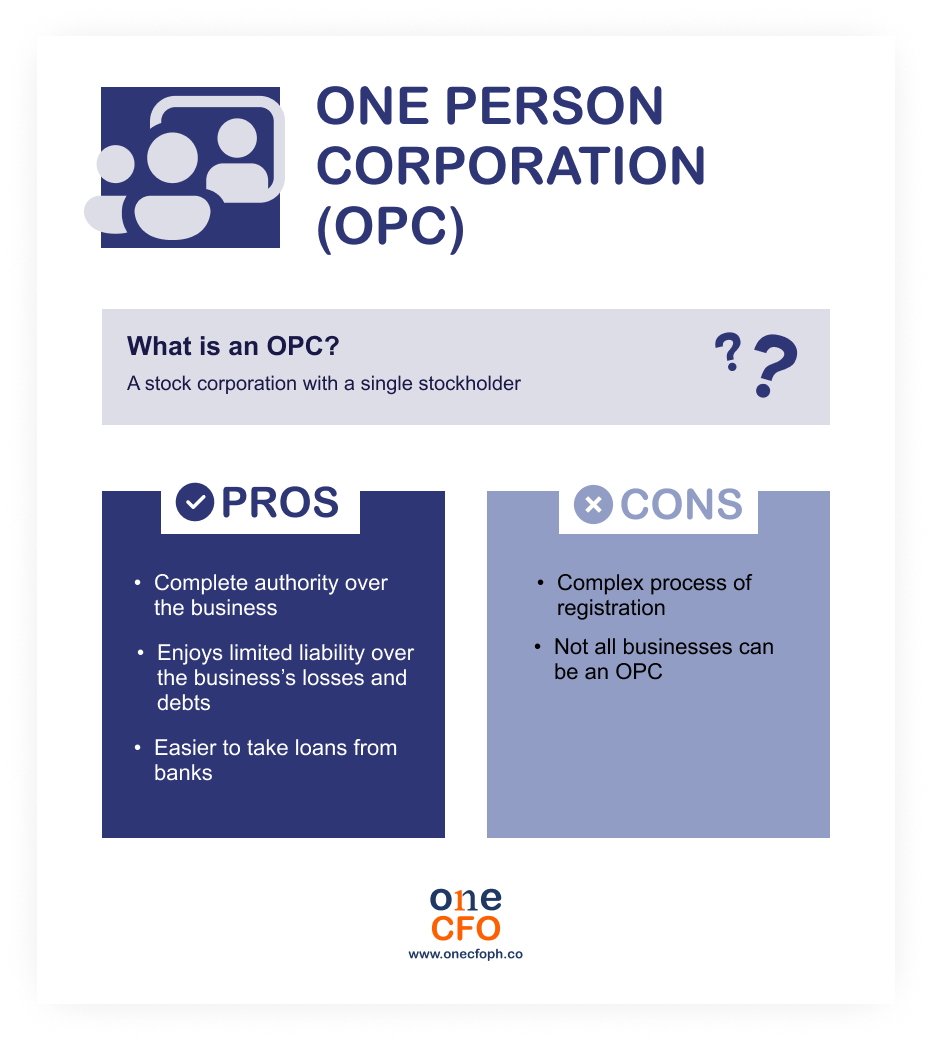

What is a One Person Corporation (OPC)?

A one person corporation or OPC is a

stock corporation with a single stockholder. This

business structure is like the incorporated version of a sole proprietorship, where the

owner enjoys complete business control but has only limited liability.

When establishing an OPC, the owner acts as the company’s director and president. The owner

needs to identify a nominee and alternate nominee, the following persons in line to run the

business if the owner can’t fulfill the duties.

Registration of this business structure is done with

the SEC. OPCs must also comply with the LGU's other requirements and register with the BIR.

Advantages of an OPC

Like sole proprietorships, the owner has complete authority over the company. The owners

mainly control all business decisions and the business's direction.

An OPC also benefits from a corporation's limited liability, which means the owner’s assets

are protected from the business’s liabilities.

Seeking funding is also easier, as the formality of a corporation lends greater credibility,

inspiring confidence among financial institutions. However, once there is more than one

stockholder in an OPC, they should convert their business structure to

a traditional corporation.

Disadvantages of an OPC

A disadvantage of OPC is its more complex registration process compared to sole

proprietorships. The additional paperwork can be a struggle, especially since the owner

operates alone.

Another con is that not all businesses can register as

OPC. Certain financial institutions

and professionals exercising their profession are not allowed to register as OPCs.

OPCs also can’t go public since it goes against the

nature of the

structure, where there’s

only one stockholder. Going public means a company can now sell shares or stocks to the

public to raise capital.

Because of these drawbacks, first-time entrepreneurs may consider a sole proprietorship as

an alternative. Check out our OPC vs Sole Proprietorship guide to compare tax implications,

compliance, and control.

How many incorporators are required for a corporation in the Philippines?

Under Philippine law, a corporation (other than a one-person corporation) must have at least

five incorporators. Each incorporator must be a natural person, and the majority of them

must be residents of the Philippines.

For an OPC, only one incorporator is needed, making it easier for solo entrepreneurs to

register.

How to choose the right business structure

Choosing the right business structure for your venture depends on your unique situation.

Consider whether you want to be a freelancer, a sole proprietor, work with a business

partner, or attract investors.

These factors will help you select the most suitable structure for your business.

Seeking funding

If you want to grow and raise capital, start with a corporation that lets you easily distribute shares to investors. Other structures can also seek funding in different ways, but are less flexible than corporations.

Control over the business

Freelancers and small business owners who want full control may prefer a sole proprietorship or a one-person corporation (OPC). These structures allow you to run the business independently while maintaining full decision-making authority.

Liability protection

Businesses like corporations and OPCs provide liability protection to their owners, which

means their assets are protected if the company suffers losses.

Partnerships may also offer the same protection if the person involved is a limited

partner.

Taxes

Each business structure has its tax compliance requirements and

rates. When assessing

potential income, it’s essential to check how the government taxes a business to determine

which option is the least expensive.

Sometimes, being a sole proprietor can be beneficial because of the 8% tax rate. However,

once you exceed the VAT threshold, being taxed as a corporation might become cheaper since

it has lower graduated

tax rates ranging from 0% to 25%.

Ease of registration

A sole proprietorship is the easiest to register since DTI has fewer requirements than the

SEC.

However, suppose your business fits more for a partnership or corporation based on the

initial factors we mentioned. In that case, going through the hoops of complying with the

SEC requirements can be more beneficial.

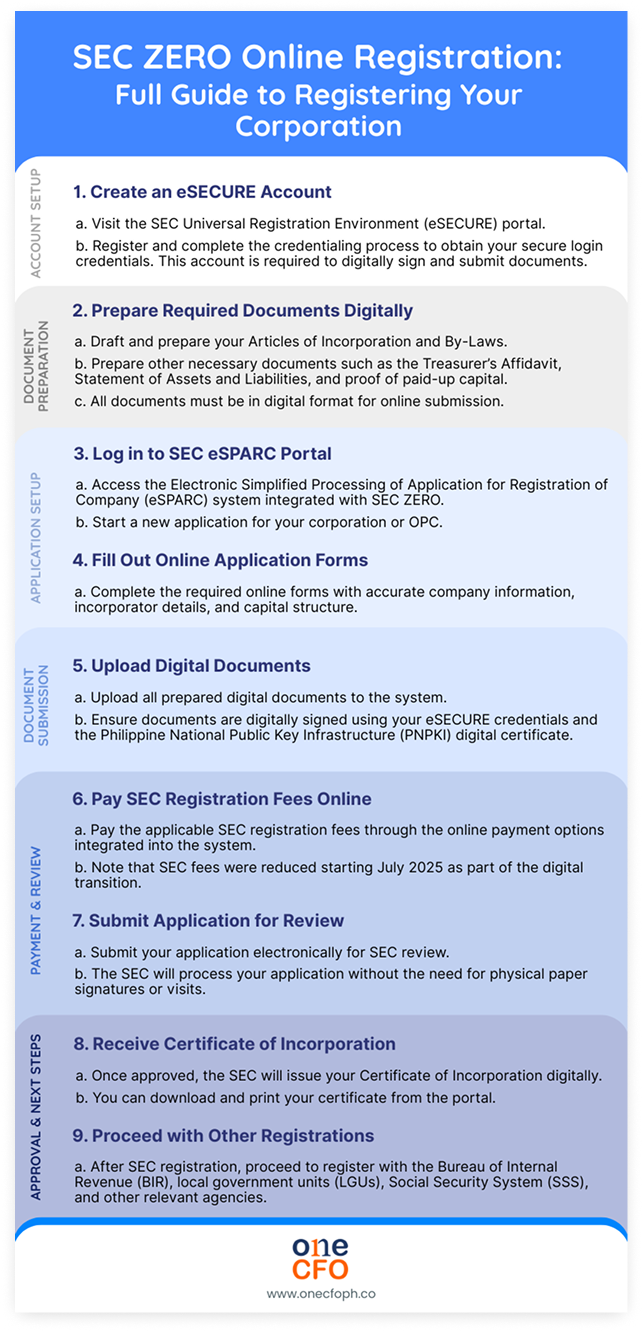

How to register a corporation online with the SEC in the Philippines

The SEC in the Philippines now requires online registration for corporations, including

OPCs. Registration is now done through the Zuper Easy Registration Online (ZERO) system by

securing an eSECURE account and completing the credentialing process to submit their

registration documents electronically.

This online process eliminates the need for physical submission and paper signatures, making

registration faster, more secure, and more convenient.

Below is the step-by-step process to register a corporation, using the SEC ZERO system:

Is SEC eSPARC the same as SEC ZERO?

No, SEC eSPARC and SEC ZERO are not the same. SEC eSPARC is the online registration portal,

while SEC ZERO is a fully digital, paperless process within eSPARC that eliminates the need

for physical documents and wet signatures.

The SEC eSPARC regular processing offers online application and payment, but still requires

the physical submission of signed, notarized documents.

SEC ZERO is designed to make company registration easier and more modern by removing

traditional paper-based steps, while eSPARC serves as the platform that facilitates both

types of processing.

Furthermore, the SEC ZERO offers a faster, more streamlined registration experience. It

handles end-to-end registration, including payment and issuance of your Certificate of

Incorporation.

Can you change your business legal structure?

Yes, you can change your business structure if it no longer aligns with your requirements as

the business expands. But it’s not a simple process.

While you can’t directly convert from a sole proprietorship to a corporation or OPC, and

vice versa, you can legally close your current business and open a new one to register the

new business entity.

Watch this video to learn more about your options in registering your business as well as

shifting to a different business structure:

Why is business registration important in the Philippines?

Registering your business is the first essential step for operating legally in the

Philippines and for building a credible, sustainable venture. It helps ensure compliance,

protects your business, and fosters trust with customers, creditors, and investors.

There are 4 legal business structures for you to choose from. Each one has different

requirements, benefits, and limitations depending on how you plan to run and grow your

business.

While online registration with the DTI and SEC has made starting a business more accessible,

many entrepreneurs still struggle with the details that matter, such as choosing the right

business structure, drafting the required registration documents, and understanding tax implications.

These are not just administrative steps. They can significantly impact your costs,

compliance, and long-term growth.

If you’re unsure where to start, getting the right guidance early on can save you time,

money, and unnecessary complications down the line.

This is where having access to fractional CFO experts can make a real difference. Beyond

registration, it’s about helping you make informed financial decisions, set up the right

structure, and build a strong foundation for your business.

At OneCFO, we don’t

just handle end-to-end business registration. We help you make

strategic, informed decisions from day one. As your business grows, our team continues to

support you with full finance services from bookkeeping, tax compliance, payroll, and

fractional CFO expertise, to help you scale with confidence.

Learn more at onecfoph.co or contact us at [email protected].

Read our disclaimer here.

About OneCFO

Based in the Philippines, OneCFO provides tech-enabled fractional CFO, bookkeeping, tax management, and payroll

support to startups, scaleups, and small- to mid-sized businesses across Southeast Asia.

We help companies manage cash flow, fundraising, and financial strategy. With our fractional CFO expertise,

business owners and finance teams gain clarity in finance and the confidence to grow.